Quick links

Registered Retirement Savings Plan

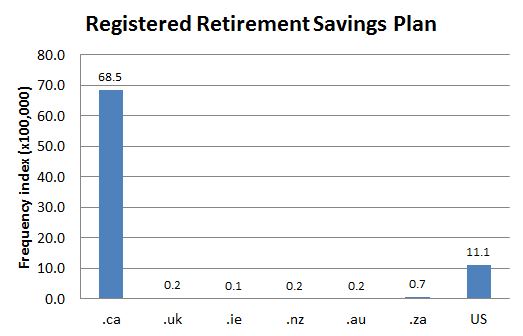

DCHP-2 (Mar 2013)

n. — Finance, Administration

a tax-deferred retirement savings plan that is registered with the Canada Revenue Agency.

Type: 1. Origin — The Registered Retirement Savings Plan was introduced in 1957 by the federal government to encourage Canadians to save privately for retirement in addition to the state pension scheme that was to become, about a decade after the introduction of the RRSP, the Canada Pension Plan. Before then, the only way to deduct pension contributions from taxable income was if the individual belonged to an employer-sponsored registered pension plan. The federal RRSP was proposed by the Liberal party under Prime Minister Louis St. Laurent (see Perry 1989 and the 1989 & 2008 quotations).

See also COD-2, which labels the term "Cdn".

See also COD-2, which labels the term "Cdn".

See: Canada Pension Plan,Old Age Security,Registered Retirement Income Fund,RRSP,Retirement Savings Plan

Quotations

1962

An investment in a government approved Registered Retirement Savings Plan affords opportunity to increase income on retirement at a preferred cost since it is deductible, up to certain limits, from 1962 earned income for income tax purposes.

1977

A Registered Retirement Savings Plan is a vehicle that allows you to set aside funds each year for retirement. Contributions to an RRSP are tax-free up to a certain limit.

1982

As a tax shelter, the RESP is not as widely known as its relatives, the registered retirement savings plan (RRSP) and registered home ownership plan (RHOSP).

1989

In the budget of 1957 the issue was finally conceded.[...] In any event the budget proposed an amendment to allow a deduction for contributions to a retirement instrument that was to be called a Registered Retirement Savings Plan. This specific allowance was to be the lesser of $2,500 or 10 percent of income, annually paid into a plan under a contract with either an annuity issuing firm or a trust company after its registration with the Income Tax Department. The proceeds of the plan were to be withdrawn as an annuity at age 65 or later, but not beyond the age of 71.

1999

Registered Retirement Savings Plans were introduced in Canada in 1957 to give Canadians an incentive to save for retirement - above and beyond their normal pension plans.

2008

But before he stepped down, Prime Minister Louis St. Laurent's government introduced what would become one of Canadians' most powerful retirement savings tools: the RRSP.

As of March 1957, the Canada and Quebec pension plans didn't exist. Only people with plans at work could deduct pension contributions for tax purposes.

2013

You should always keep fixed income inside your RRSP.

This is a widely accepted rule of thumb that has important implications for dividend investors. It holds that, because interest is taxed at your marginal rate while dividends and capital gains are taxed at lower rates, you should keep fixed income inside your RRSP and leave stocks outside (assuming you don't have room for both).

2016

If you and your spouse earn different levels of income, a spousal RRSP may be an effective way to "split income" over the long term. To do so, the spouse who is expected to have a higher level of income at retirement should make the contribution to a spousal RRSP. This will allow you to build a nest egg that will provide each of you with a source of income in retirement and an overall reduction in taxes.

References

- Perry (1989)

- COD-2

Images